In July 2025, the U.S. auto market delivered a better-than-expected performance: sales volume reached 1.37 million units, with the seasonally adjusted annual rate (SAAR) hitting 16.4 million units—up 6.6% year-on-year and 7.1% month-on-month. Against the backdrop of intertwined challenges like high interest rates, rising prices, and tariff uncertainties, these figures stand out remarkably.

Light-duty trucks remained the main driver of growth, accounting for a staggering 84% of total sales. For consumers, factors such as space, functionality, and diverse energy options continued to be the core considerations when purchasing a vehicle. Part of the sales growth stemmed from the combination of policy expectations and cyclical factors—advance purchases triggered by pending tariff uncertainties, and the low comparison base caused by system failures last year.

The recovery in July this year is more like a rebound after correcting fluctuations. The electric vehicle (EV) segment showed complex divergence: hybrid vehicles saw rapid growth, plug-in models appeared slightly sluggish, and battery electric vehicles (BEVs) maintained their market share but lacked breakthroughs.

In July 2025, the SAAR of the U.S. auto market reached 16.4 million units, a significant increase from June and also higher than the 15.8 million units in the same period of 2024.

Light-duty trucks were the primary driver of this growth, making up 84% of sales. Models such as pickup trucks and SUVs remained American consumers’ top choices due to their space, functionality, and diverse energy options. In sharp contrast, sedan sales continued to decline and are being further marginalized.

This round of growth is not entirely driven by natural demand:

On one hand, part of the sales volume resulted from "advance release." Due to earlier tariff policy uncertainties, sales from March to April included advance purchases, and the July recovery is to some extent a correction for the fluctuations in the first half of the year.

On the other hand, a software system failure last year affected some sales data, making this year’s year-on-year growth rate appear more prominent.

The high-interest-rate environment has significantly increased the cost of auto loans, putting greater pressure on consumers to purchase vehicles.

Tariffs have driven up the costs of both finished vehicles and auto parts, making it difficult to lower end-user prices and suppressing demand from price-sensitive consumers.

Even so, automakers’ incentive measures remain below historical averages. This reflects the cost pressures faced by manufacturers themselves and also indicates that the market has not yet entered a state of over-reliance on subsidies for stimulation.

From an operational perspective, the July recovery is the result of overlapping factors: resilient demand, policy expectations, and sales cycles. However, this does not mean the trend will be sustainable in the future.

If tariffs continue to increase, the impact will be further passed on to vehicle prices.

If there is no substantial improvement in credit conditions, consumer potential will remain constrained.

While the broader U.S. auto market rebounded in July 2025, the electric vehicle (EV) segment

In July 2025, hybrid electric vehicles (HEVs) achieved 160,000 sales in the U.S., marking a nearly 20% year-on-year surge—the most notable growth within the new energy vehicle (NEV) category.

Toyota remained the dominant player, capturing over 40% market share through its winning formula: lower prices, mature hybrid technology, and convenience of no external charging. This strategy successfully attracted cost-conscious consumers prioritizing fuel efficiency

The growth of hybrid models exemplifies the gradual transition in the U.S. market toward electrification. As consumers balance affordability, infrastructure readiness, and environmental goals, hybrid vehicles serve as a pragmatic bridge technology. This aligns with Toyota’s global strategy of positioning full hybrids (HEVs) as the cornerstone of its electrification roadmap, aiming for 70% HEV sales in Europe by 2025 and similar penetration in key markets like the U.S..

While pure EVs face challenges like high interest rates on auto loans and tariff-driven price pressures, hybrids benefit from lower ownership costs and proven reliability. The July performance underscores that, for many American buyers, electrification remains a step-by-step journey rather than an abrupt shift.

In contrast, plug-in electric vehicles (PEVs) showed relatively weak momentum: total PEV sales in July reached approximately 135,000 units, a 1.1% year-on-year decline—a lackluster performance amid the overall market growth.

Among these, battery electric vehicles (BEVs) accounted for around 113,000 units, while plug-in hybrid electric vehicles (PHEVs) made up roughly 21,000 units.

BEVs held a 9.9% share of the overall monthly market, continuing their recent trend of hovering near the 10% mark. Considering BEVs accounted for 9.9% of total sales throughout last year (a slight increase from 9.4% in 2023), their penetration rate is rising slowly. However, high prices, uneven charging infrastructure distribution, and policy uncertainties remain the main barriers to further growth. Fuel cell vehicles (FCVs) remained marginal, with only 37 units sold in July.

In July 2025, the U.S. EV market saw robust growth, driven by policy incentives and immediate consumer demand.

With the tax credits under the Inflation Reduction Act (IRA) approaching expiration, a "rush to purchase" emerged in the market. Both new and used EV sales surged significantly in July, pushing the EV market to a short-term peak. However, this also introduced complex variables for the market’s stability moving forward.

Tesla maintained its dominant position with 53,816 units sold.

Traditional automakers such as Chevrolet, Hyundai, Ford, and Honda also delivered strong results. Notably, Volkswagen saw a 454% year-on-year increase, jumping directly to the 6th place in sales rankings.

Luxury brands like Audi (+150.2%), Cadillac (+14.5%), and Mercedes-Benz (+6.4%) also posted growth.

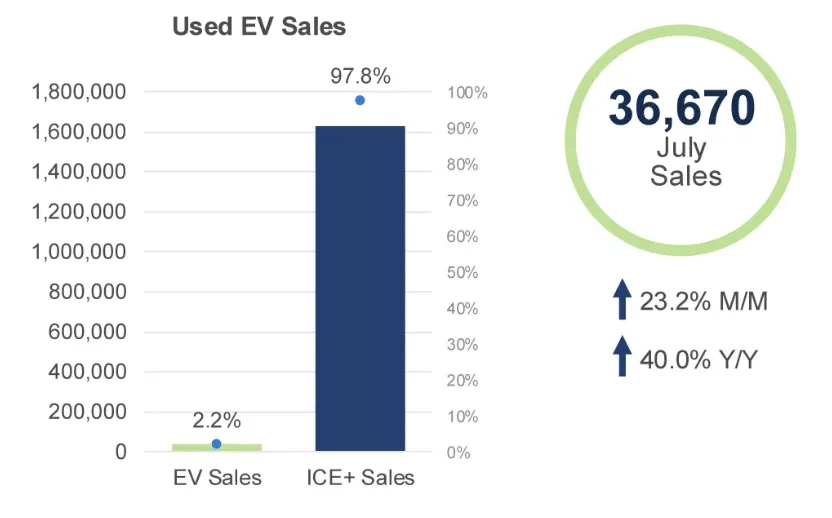

The used EV market remained equally buoyant:

Used EV sales rose to 36,670 units in July, up 23.2% month-on-month and 40.0% year-on-year, accounting for 2.2% of the total used car market.

Tesla remained the leading player but saw its market share drop from 45.2% in June to 43.4%. Brands including Honda (+103.0%), Hyundai (+61.3%), and Rivian (+60.5%) recorded rapid growth.

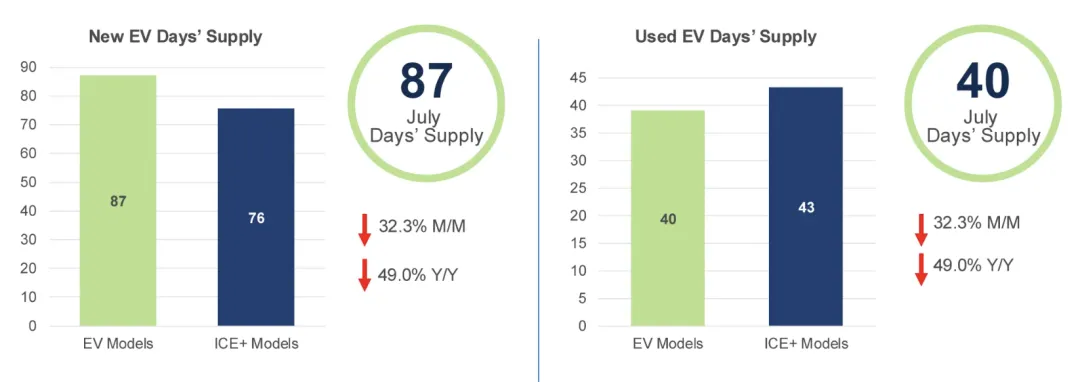

On the supply front, the market is grappling with intensified tensions. New electric vehicle (EV) days’ supply plummeted to 87 days in July, marking a 32.3% month-over-month decline and a 49.0% year-over-year drop . This reduction narrowed the gap with internal combustion engine (ICE) vehicles to just 11.6 days—the smallest margin in six months—as EVs accelerated de-stocking efforts and approached ICE-level inventory turnover efficiency .

Audi retained the highest days’ supply at 168 days, though this represented a significant improvement from prior months.

Toyota demonstrated the tightest supply-demand balance with only 42 days’ supply, highlighting its streamlined production-consumption alignment .

The used EV segment faced even sharper constraints:

Days’ supply fell to 40 days, continuously below ICE vehicles for five consecutive months .

Tesla, Chevrolet, and Nissan led the charge in rapid inventory turnover, creating a "supply-constrained frenzy" where high demand outpaced available stock . This dynamic left consumers struggling to secure vehicles, with some models facing waitlists.

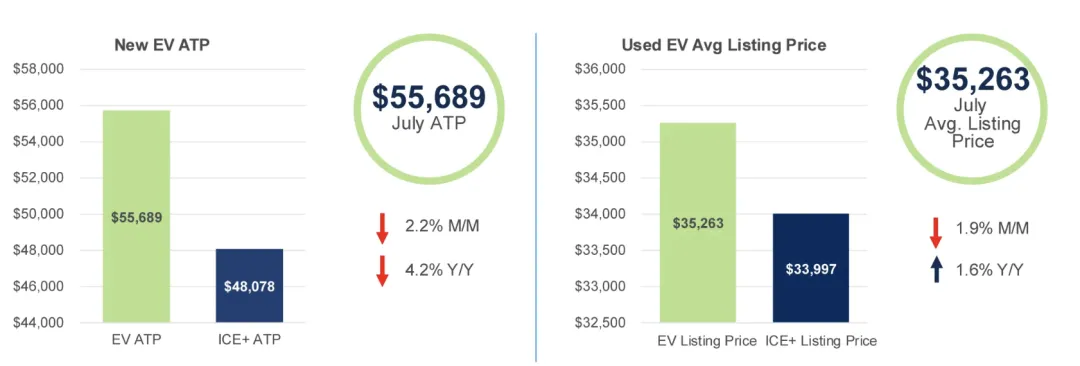

The average transaction price (ATP) for new electric vehicles (EVs) plunged to $55,689 in July, marking a 2.2% month-over-month decline and a 4.2% year-over-year drop . This narrowed the price gap with internal combustion engine (ICE) vehicles to $7,611—the smallest margin in nearly a year. The price correction was primarily driven by automakers’ aggressive sales push ahead of potential tariff adjustments and heightened subsidy-driven demand .

EV incentives rose for the fourth consecutive month, reaching 17.5% of the sale price (equivalent to $9,768)—the highest level in the history of EV sales . This surge reflects automakers’ strategic use of discounts to counterbalance high interest rates and price-sensitive consumer behavior. For instance:

Volvo led price cuts with a 17.1% reduction, followed by Volkswagen at 12.2% .

Tesla maintained its dominance by offering targeted Model Y/3 rebates, despite holding premium pricing positions.

In the top-five best-selling EV models, Tesla Model Y and Model 3 continued to dominate, accounting for over 60% of total EV sales . Their success stems from:

Balanced pricing ($40,000–$55,000 range)

Expanded Supercharger network accessibility

Strong residual value retention

Notably, used EV prices also stabilized at 87% of new vehicle ATP, signaling improved market maturity. The Tesla Model Y alone captured 43.4% of the used EV market share, though competitors like Hyundai IONIQ 5 (+61.3% YoY) are gaining traction .

In July, the average listing price for used electric vehicles (EVs) dropped to $35,263, a 1.9% month-over-month decrease. Though it still rose 1.6% year-on-year, the price gap between used EVs and internal combustion engine (ICE) vehicles narrowed to a historic low of just $1,266.

Tesla maintained its pricing leadership in the used market: the average prices of the Model 3, Model Y, and Model S remained significantly below the overall used EV market average, thanks to strong residual value retention and high consumer demand.

The EV market is likely to maintain strong growth for the remainder of Q3, especially as the "pre-policy expiration rush"—driven by the upcoming end of IRA tax credits—shows no signs of abating.

However, as subsidies gradually phase out, the market’s sustainability will hinge on two key factors:

Whether automakers can strike a new balance between price and value to retain cost-sensitive consumers;

Whether the supply-demand dynamic can continue to improve, preventing volatility after the current sales boom.

July’s market prosperity was largely numbers-focused—underlying challenges like high interest rates, tariff pass-through to vehicle prices, and persistent cost pressures still loom over the industry.

The new energy vehicle (NEV) segment serves as a telling barometer:

The growth of hybrid vehicles highlights that consumers remain sensitive to cost and convenience;

The stagnation of battery electric vehicles (BEVs) reflects that infrastructure gaps and pricing remain critical bottlenecks.

As IRA tax credits gradually exit, the U.S. EV market will face a true test. It will likely see a final sales sprint in the last two months of the year, followed by a period of rebalancing to align with fundamental market logic.