News Center

Analysis of the European Automotive Market in Q1 2025: Accelerated Electrification

In the first quarter of 2025, new car registrations in the EU fell 1.9% year-on-year. The market share of battery electric vehicles (BEVs) rose from 12% in 2024 to 15.2%, reflecting the accelerated trend of electrification in Europe. Hybrid electric vehicles (HEVs) continued to lead the market with a 35.5% share, becoming consumers’ top choice, while the market share of traditional gasoline and diesel vehicles dropped significantly to 38.3%.

Across the European market, sales of BEVs, plug-in hybrid electric vehicles (PHEVs), and HEVs reached 573,500 units, 267,500 units, and 1,214,700 units respectively, with total vehicle sales at 3.382 million units.

Part 1

Accelerated Electrification Trend: Dual-Drive Growth in BEV and HEV Markets

The EU automotive market demonstrated significant growth momentum in electrification during Q1 2025, particularly driven by battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs). The analysis below covers market data, regional performance, and key drivers.

● Battery Electric Vehicles (BEVs)

- BEVs achieved a 23.9% year-on-year sales increase in Q1 2025, with registrations reaching 412,997 units.

- Their market share rose from 12% in the same period of 2024 to 15.2%, fueled by strong performance in core markets such as Germany (+38.9%), Belgium (+29.9%), and the Netherlands (+7.9%).

Regional Highlights:

- Germany, the largest automotive market in the EU, saw explosive BEV sales growth primarily driven by European automakers’ efforts to meet carbon emission regulations.

- Belgium and the Netherlands** witnessed growth linked to tax incentives and rising demand for electrified corporate fleets.

- France experienced a 6.6% sales decline due to consumers’ price sensitivity toward EVs and uneven distribution of charging infrastructure.

● Plug-in hybrid electric vehicles (PHEVs) saw a 1.1% year-on-year increase in registrations, reaching 207,048 units, with market share edging up from 7.4% to 7.6%. Significant growth in Germany (+41.8%) and Spain (+30.7%) drove this trend, while other markets remained relatively stable.

PHEV growth lagged behind BEVs and HEVs, likely due to their higher purchase costs and technical complexity. However, in markets with strong policy support like Germany, PHEVs remained popular among enterprises and premium consumers.

**PHEV Sales in Q1 2025:**

In Germany, PHEV sales reached 64,000 units in Q1 (18,000 in January, 20,000 in February, and 27,000 in March). The UK sold 54,000 units (13,000 in January, 7,000 in February, and 34,000 in March). Spain recorded 21,000 units (5,000 in January, 7,000 in February, and 8,000 in March), while France sold 20,000 units (5,000 in January, 6,000 in February, and 9,000 in March). Italy and Sweden sold 19,000 units and 16,000 units respectively. The Netherlands and Belgium sold 16,000 units and 10,000 units, while Ireland and Portugal sold 9,000 units and 7,000 units. Other regions combined sold 32,000 units, bringing the total PHEV sales in Q1 to 268,000 units.

● Hybrid electric vehicles (HEVs) remained the EU market leader with a 35.5% share, achieving a 20.7% year-on-year increase in registrations to 964,108 units in Q1 2025. Strong growth in France (+47.5%), Spain (+36.6%), Italy (+15.3%), and Germany (+10.5%) drove this trend.

HEVs’ popularity stems from their balance of fuel efficiency and electrification technology, particularly appealing to consumers concerned about BEV range or charging accessibility. Their advantages in technological maturity and price competitiveness have made them a mainstream choice during the transitional period, especially in price-sensitive markets like Spain and Italy, where lower purchase and usage costs make them preferable.

● The growth of the electrified market stems from multiple factors:

◎ Strict EU carbon emission regulations (such as the Euro 7 standard) and government purchase subsidies have incentivized consumers to switch to electric vehicles.

◎ The continuous expansion of charging infrastructure has alleviated "range anxiety," with Germany and the Netherlands adding大量 (large numbers of) public charging piles in 2024, significantly enhancing EV usability.

◎ Automakers have increased investments in EV market promotion and launched more affordable models, further stimulating demand.

Despite this, the 15.2% BEV market share still fell short of expectations, hindered by high purchase costs, insufficient charging accessibility, and consumer perception gaps. In markets like France, uneven policy implementation and economic uncertainties have slowed EV adoption.

Part 2  Sales of Major Automotive Groups

● January–March 2025, European automotive market:

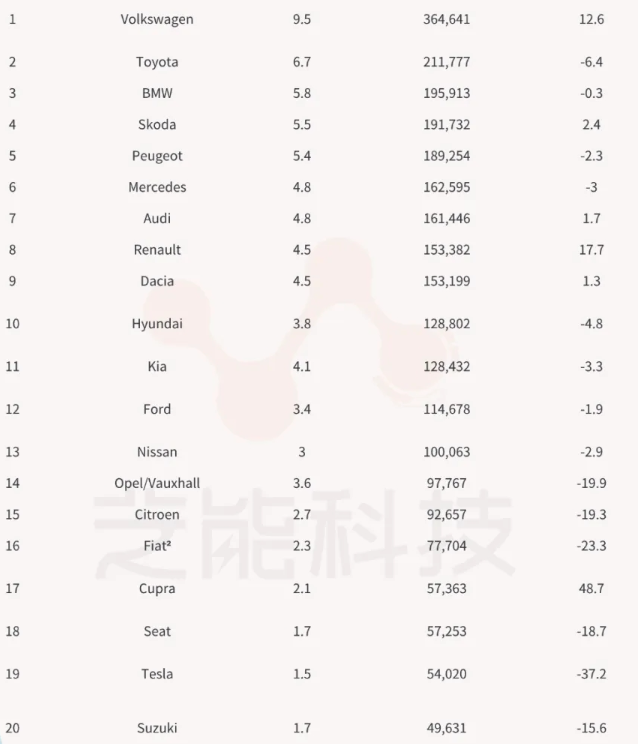

◎ Volkswagen Group maintained its lead with a 25.9% market share, selling 875,875 vehicles (+5.7% YoY).

◎ Stellantis Group held a 15.5% share, selling 725,283 vehicles (-12.2% YoY).

◎ Renault Group stood out with a 10.2% share and 344,519 vehicles sold (+10% YoY).

◎ Hyundai Group (7.9% share, 267,234 vehicles, -4% YoY) and Toyota Group (7.4% share, 227,863 vehicles, -4.4% YoY) both experienced sales declines.

◎ BMW Group (6.8% share, 236,401 vehicles, +0.5% YoY) saw marginal growth.

◎ Mercedes-Benz (4.9% share, 165,518 vehicles, -5.4% YoY) and Jaguar Land Rover (1.3% share, 41,430 vehicles, -7.9% YoY) recorded sales drops.

◎ Volvo Cars (2.5% share, 83,092 vehicles, +9.9% YoY) and SAIC Group (2.3% share, 78,505 vehicles, +33.5% YoY) achieved strong growth.

◎ Tesla sold 54,000 vehicles (-37.2% YoY).BEV Sales in Q1 2025:

In Germany, BEV sales reached 113,000 units in Q1 (34,000 in January, 36,000 in February, and 43,000 in March). France sold 75,000 units (20,000 in January, 25,000 in February, and 29,000 in March). The UK recorded 120,000 units (30,000 in January, 21,000 in February, and 69,000 in March). Belgium sold 40,000 units (14,000 in January, 13,000 in February, and 14,000 in March), while the Netherlands sold 32,000 units (11,000 in January, 10,000 in February, and 11,000 in March). Norway, Denmark, Italy, Sweden, and Spain sold 29,000 units, 25,000 units, 23,000 units, 21,000 units, and 19,000 units respectively in Q1. Other regions combined sold 77,000 units, bringing the total BEV sales in Q1 to 574,000 units. In the first quarter of 2025, the EU automotive market showed a stark polarization: the electrification wave drove the rapid growth of battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs), while the traditional gasoline and diesel vehicle market shrank rapidly.

The market share of BEVs reached 15.2%, with HEVs leading at 35.5%. Germany, Belgium, and the Netherlands demonstrated strong performance in the EV market, while the sales decline in France highlighted regional disparities in policy implementation and market maturity. The rapid contraction of the traditional fuel vehicle market has created space for electrification transformation, but it also brings challenges in supply chains, employment, and economic stability.

Sales of Major Automotive Groups

● January–March 2025, European automotive market:

◎ Volkswagen Group maintained its lead with a 25.9% market share, selling 875,875 vehicles (+5.7% YoY).

◎ Stellantis Group held a 15.5% share, selling 725,283 vehicles (-12.2% YoY).

◎ Renault Group stood out with a 10.2% share and 344,519 vehicles sold (+10% YoY).

◎ Hyundai Group (7.9% share, 267,234 vehicles, -4% YoY) and Toyota Group (7.4% share, 227,863 vehicles, -4.4% YoY) both experienced sales declines.

◎ BMW Group (6.8% share, 236,401 vehicles, +0.5% YoY) saw marginal growth.

◎ Mercedes-Benz (4.9% share, 165,518 vehicles, -5.4% YoY) and Jaguar Land Rover (1.3% share, 41,430 vehicles, -7.9% YoY) recorded sales drops.

◎ Volvo Cars (2.5% share, 83,092 vehicles, +9.9% YoY) and SAIC Group (2.3% share, 78,505 vehicles, +33.5% YoY) achieved strong growth.

◎ Tesla sold 54,000 vehicles (-37.2% YoY).BEV Sales in Q1 2025:

In Germany, BEV sales reached 113,000 units in Q1 (34,000 in January, 36,000 in February, and 43,000 in March). France sold 75,000 units (20,000 in January, 25,000 in February, and 29,000 in March). The UK recorded 120,000 units (30,000 in January, 21,000 in February, and 69,000 in March). Belgium sold 40,000 units (14,000 in January, 13,000 in February, and 14,000 in March), while the Netherlands sold 32,000 units (11,000 in January, 10,000 in February, and 11,000 in March). Norway, Denmark, Italy, Sweden, and Spain sold 29,000 units, 25,000 units, 23,000 units, 21,000 units, and 19,000 units respectively in Q1. Other regions combined sold 77,000 units, bringing the total BEV sales in Q1 to 574,000 units. In the first quarter of 2025, the EU automotive market showed a stark polarization: the electrification wave drove the rapid growth of battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs), while the traditional gasoline and diesel vehicle market shrank rapidly.

The market share of BEVs reached 15.2%, with HEVs leading at 35.5%. Germany, Belgium, and the Netherlands demonstrated strong performance in the EV market, while the sales decline in France highlighted regional disparities in policy implementation and market maturity. The rapid contraction of the traditional fuel vehicle market has created space for electrification transformation, but it also brings challenges in supply chains, employment, and economic stability.

LED driver power supply

New energy vehicle charger